What is the difference between MiFID and IDD Licenced Advisers?

Why licencing affects your consumer protectionsAuthor: James Pearcy-Caldwell

A firm with an investment licence typically has the authorisation to buy, sell, and manage investments on behalf of clients.

On the other hand, a firm with an insurance licence primarily deals with insurance products. It can sell and manage insurance policies such as life insurance, health insurance, property and casualty insurance, and more. Their focus is on mitigating risk and providing financial protection against specific unforeseen events. This is known as an IDD licence.

The key distinction lies in the primary financial products and services firms are licenced to offer: investment firms handle investment instruments and strategies, while insurance firms deal with various insurance products for risk management and protection. However, some financial firms might have licences for both investment and insurance products, allowing them to provide a broader range of financial services.

Why is this important?

Understanding the distinction between firms with investment and insurance licences is crucial for a few reasons:

- **Financial Services Selection: Knowing the type of licence a firm holds helps individuals or businesses choose the right service provider. If someone needs investment advice or wants to purchase securities, they would approach a firm with an investment licence. Conversely, for insurance-related needs, they’d seek out a firm with an insurance licence.

- **Regulatory Compliance: Financial firms need to comply with specific regulations tied to their licences. These regulations are designed to protect consumers and ensure the proper handling of financial transactions. Understanding which licence a firm holds can give insight into the regulatory framework under which it operates.

- **Scope of Services: Different licences allow firms to offer different services. Knowing the scope of services a firm can provide helps clients understand the limitations and capabilities of the firm. This informs the type of assistance or products one can expect from the firm.

- **Risk and Protection: The services offered by each type of firm cater to different aspects of financial health. Investment firms help individuals grow wealth through strategic investment, while insurance firms focus on protecting against financial loss due to unforeseen events. Understanding this helps individuals make more informed decisions about how to manage their finances and mitigate risks.

Knowing the difference between these types of firms is crucial for making informed decisions about managing one’s financial future and for engaging with the appropriate professionals to meet specific financial needs.

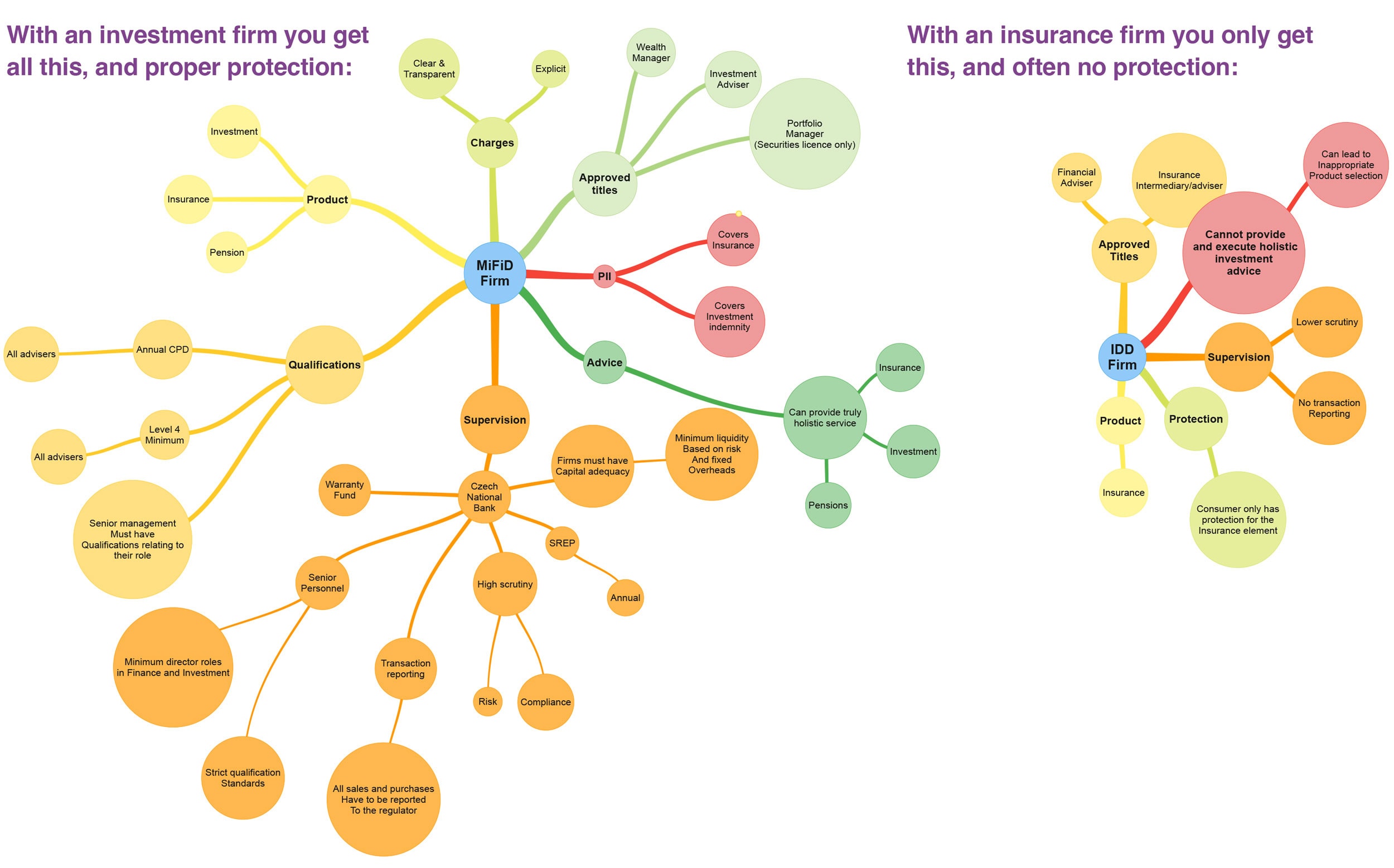

Investments and Investment advice have limited or no regulatory cover with IDD firms in the European Union

When dealing with an IDD only adviser firm consumers should be aware:

- No Warranty Fund exists

- Lower capital adequacy and lesser qualifications apply

- Lower level of regulatory supervision exists

- PII cover is unlikely to cover investments nor investment advice

- Lower level of consumer protection for the investing public

- If a company goes bust no protection for the investments

This means as a retail client of an IDD only firm you:

- Have no recourse to complain to an Ombudsman linked to the IDD firm, nor pension trustees;

- will not be covered by MiFID firm warranty funds (Your IDD adviser has no such protection);

- will not, for most model portfolios, have any recourse to complain to the DIM or its regulators;

- will not, within an insurance bond (including SIPP and QROPS), be covered by any warranty fund.

Effectively, if you were to be advised by an IDD only firm in an insurance product (incl. pensions), you would not have any complaints resolution available, lose consumer protections and EU investor compensation schemes and the IDD firm is unlikely to have valid investment PII insurance.

| MiFID & IDD in one firm | IDD only |

|---|---|

| PII which legally has to provide both insurance and investment indemnity cover | PII provides no investment indemnity cover or protection to clients |

| Warranty Fund to protect consumers (Compulsory) | Warranty Fund does not exist |

| Firms must have capital adequacy and minimum liquidity based on risk and fixed overheads | No capital adequacy or liquidity standards and no risk nor fixed overhead requirements (Firms can be valued as little as €37,000) |

| Annual SREP stands for Supervisory Review and Evaluation Process |

No Supervisory Review and Evaluation Process |

| Strict qualification standards required of senior personnel and compliance | Lower qualification standards required of senior personnel or supervisor |

| Minimum qualification standard for each investment adviser (individually) | No required qualification standard for each individual insurance adviser in most EU countries |

| MiFID standard transparency on investments with PRIIP reporting on insurance | Lower standards based only on PRIIP reporting on insurance and insured funds |

| Third country pension schemes (specifically Malta and UK) require a MiFID licence | Not approved to advice on third country pensions (must recommend another suitably qualified firm) |

| What is covered? | What is covered? |

| Both Investment advice, and investments within insurance and pension products are covered | Insured investments within insurance and some EU pension products are covered (if they have a supplementary pensions licence) |

| What is supervision? | What is supervision? |

| High scrutiny from the regulator is required, linked to risk and compliance | Far lower scrutiny from the regulator |

| Transaction reporting – all sales and purchases have to be reported under ISA 20022 to the regulator | No transaction reporting |

| Approved titles? | Approved titles? |

| Wealth Manager Investment Adviser Portfolio Manager (Security trader licence only) |

Financial Adviser Insurance Intermediary / Adviser |

| How is the consumer protected? | How is the consumer protected? |

| The consumer has a full suite of protection on both investments and insurance policies based on regulatory requirements (warranty and PII) thorough to complaints and whistle blowing processes and published terms of the company. |

The consumer has limited protection on insurance policies only (PII) and the only investments are available through insurance bonds. |

| Charges are explicit and third country pension schemes are protected advice under MiFID. |

No MiFID advice is protected on any investments by the IDD company or representative even where a third party firm offers it. |

Use of Non-EU investment firms via an IDD (insurance) licence (what it means for consumers)

- No Warranty Fund in EU

- Lower capital adequacy and lesser qualifications

- Lower level of regulatory supervision

- PII cover is unlikely to cover investments nor investment advice

- Lower level of consumer protection for the investing public

- If a company goes bust no protection for the investments

- No annual SREP Review